|

|

Quote:

Quote:

Which of these is more typical? Is it just that Jim has an insanely inexpensive plan (my share of the plan I get through my company is about $210/mo for family coverage; I do not know what the company is paying, but I assume it's something) and costs overall are evening out? Obviously that sucks for Jim (and those like him -- regional thing?) but I'm not sure that proves anything about the plan overall. |

Quote:

I can think of a pretty sizable portion of the population that would prefer policies that don't offer maternity care. Not that I don't believe the results, but I am surprised by Jim's offer of an 8.5K out of pocket -- I thought cost sharing needed to be limited to HSA limits, which are around 6K. Also, did the deductible change? |

I don't know the global answer. I know here in Maine the situation for self-employed people, as I've said earlier in the thread, is much more like Radii's. The Affordable Care plans are much much better than what was currently available.

|

Quote:

Man I love that line, it has everything. It is the best example of an anecdotal proclamation of truth I've ever read. For me, I will start using "Isnfpetmmoitr" in posts. |

Quote:

Probably somewhere in between. I got dinged for weight when I first signed up. I had no other options but BCBSNC (all commercial payers like United/Aetna/Humana declined to offer me coverage) and BCBSNC made it clear I was being charged a premium. When I first signed up I paid ~$425/mo. Over the last 5 years its gone up every year to the current $625. For income tax purposes, I do get to deduct 100% of my premiums, so the effective cost is a little lower as a result. |

Catastrophic plans have tended to be complete and utter shit in two ways.

The first is in benefits offered, but that's OK since most who buy a catastrophic plan don't intend to use "regular" benefits. This, however, is bad for society (see below). The second, however, is in the ways the company that offers the plan tends to have to get out of actually living up to your expectations should you actually need catastrophic coverage. Kinda sucks to be on your way to the hospital and find out you're not going to be covered, at all, because of some fine print. At the private health insurance company I worked at until recently (one of the 5 largest in the United States), the doctors who ran the Care Management division hated catastrophic plans. The reason was that those with these plans tended to avoid treatment for anything for so long that by the time they showed up, they cost a fortune to treat, usually in a losing cause as well. So basically the existence of catastrophic plans enables (and even encourages) the misuse (through non-use, then overuse) of medical treatment options. In addition, many with these plans will cost the taxpayer a lot of money should they (and they are) dropped from coverage once they have an expensive condition (see: lawyers). The irony is that even private insurance companies want you to use your benefits. Using your benefits means you tend to cost a lot less in the long run, which is better for everyone, not just the docs and nurses in Care Management, but the C-Suite looking at the margins. (I'd like to note that I'm not accusing Jim or anyone else here who may have had catastrophic plans as being part of the problem. I'm going to assume all FOFC people are smart people who keep themselves healthy and seek treatment in a timely manner when necessary.) I'll leave you with an anecdote about this. When I worked for this company, we took on an employer group in an urban area who had a very large blue collar staff. These employees, by and large, had never had private health insurance before, but the employer wanted to finally offer it to them. The concern we had, as a company, was how we would get these folks, who were used to, at best, using the ER for any and all medical treatment, to actually use the benefits they were going to have, which included preventative care, checkups, wellness, etc.... In the end they decided to use part of the budget to hire several nurses who lived in the area, and task them with calling, educating, explaining, etc... these new members on how to use their health benefits, including everything from finding a PCP (including explaining what a PCP was), how to schedule an appointment (and for what), etc.... Having done the research on similar populations, it was an easy decision to approve, as it was clear the short-term cost would be far-less than the long-term cost of not getting these folks to use their benefits. |

It's frustrating to read that my decision, which is to pay for the medical treatment I need, is somehow selfish or un-American or utter shit. I haven't been to an emergency room for a long time. It's not something I'd use except in an emergency.

If you have low-level insurance, by the way, it's a fairly stupid way to handle health care anyway - you still pay until you reach a deductible, and emergency rooms are more expensive than a regular doctor visit. What is insurance? Budgeting an amount of money to protect you from bankruptcy should something bad happen. We don't have home insurance to pay for, let's say, a new water heater when your old one breaks down. We have it for the small percentage chance of a fire or a tornado or something along those lines. We don't expect our auto insurance company to cover us for an oil change every 5,000 miles. We can educate people on the value of having a physical exam every year or so. Some insurance companies, on their own, even added this to catastrophic plans as it can save them money in the long run. But that's not even what this debate is about. It's about the government taking over health insurance and turning it into something different. I have my selfish un-American utter-shit insurance. Obviously, I'd like one of those employer-paid packages with concepts like co-pays, but that's an expensive benefit and that kind of insurance isn't available for self-employed people - at least not at less than $1,000 a month. Sure, my utter-shit insurance doesn't pay anything if I get pregnant, but I think I can handle the risk of pregnancy on my own. My insurance is there to ensure that I get decent medical care in the event of a serious illness. With Obamacare, I will pay three times as much to get an inferior product. With Obamacare, if I have a serious illness, I can only receive treatment from in-network doctors. And, really, there's no guarantee that there will be any in-network doctors for many specialties. That's my biggest concern. With Obamacare, I cannot keep my old insurance and I cannot chose my own doctor. How many people would have supported this plan had they known that Obama's campaign promises were utter bullshit? There's a reason even unions are against Obamacare now that some of the problems are being exposed. Obviously, selfish utter-shit insurance wasn't available everywhere. There are many states where regulations have kept high-deductible plans out of the marketplace for the self-employed. So this has some value, though real health care reform would have been a better solution. And, of course, if you qualify for the subsidies, which means other people pay for your health care, then it has more value. But don't forget that real costs are still being incurred and someone else is paying for them. |

Quote:

I haven't been a part of these debates very frequently so I don't know what's been discussed in here before... but I am curious if you are aware of how much of our nation's insurance is already "taken over by the government" ? I work for a healthcare technology company with services in a few hundred medical offices around the country from hospitals to primary care offices to specialist offices. Our software manages patient check-in's, so every appointment goes through our system. Last time I checked, 38% of our volume was for Medicare patients. I think another 10-15% are Medicaid. Government *already* runs at least half the healthcare in the country. No one but the heaviest tea partiers or libertarians even want to reduce that. We love the government being involved in our healthcare. Quote:

The best insurance you could get as an individual was $1000/mo that wasn't a catastrophic plan? See my above posts where I am deemed a health risk and originally got insurance for less than half that a few years ago, I have my problems with it for sure, but because of my health risk it was worth it to pay, so I did. It wasn't for you, so you didn't. But I'm calling a very high level of bullshit on this. Quote:

Have you researched this for yourself? You get to do that before you commit to anything. The people who are freaking out about in network providers are typically ones that have long term relationships with specific providers and are afraid of their network being slightly smaller than it is today. It sounds like you've taken good care of yourself and have been lucky to not need a lot of care, I wouldn't have thought you were in the group impacted by this. The articles I've read talk about some payers limiting some provider networks by 10-20% to help keep costs down for patients, in some plans (but still offering more expensive plans with the same options generally). Are there serious concerns that "my plan forgot to contract with a cardiologist in my region, so I guess I'm screwed" ??? Quote:

This is of course the big political question, and I'm clearly on the other side of it, but I'll remind everyone here that we are already doing this in a monumental way, and if anyone seriously suggested we stopped, most of us, even those who violently oppose Obamacare, would absolutely lose their shit. |

Quote:

So, why not just eliminate health insurance entirely? Why continue to create winners and losers? Quote:

Yes, there's a heap of bullshit you can place on a straw man. Always is. That's why people create straw men. The value of many employer-paid plans is over $1,000 in the private market. That's not even available to the self-employed in many states. Let's say you're a teacher. The average cost of insurance for teachers, nation-wide, is more than $700 per month - as part of a very large group. It's certainly not a stretch to say that many individuals would have to pay $1,000 for that level of coverage, since the self-employed don't get the benefits of being in that large a group. I'm sure there's a level of insurance out there I would have to pay $1,000 to receive. The Gold plan would cost me $480. But again, that has no out-of-network coverage. Quote:

We don't know what will be in-network and what won't be under Obamacare. There are plenty of doctors who aren't in-network today. Their payments in many cases will be lower under Obamacare, so it stands to reason that more will refuse to participate. Under Obamacare, you're not covered out of network, period. That's a real, tangible reason that it's a lower level of coverage than the high-deductible plans so many here are calling utter shit. And, yes, I've discussed this with the company I use to price insurance. Their advice is to stay out of the exchange as long as possible unless I qualify for Medicaid, which I don't (Of course, if FOF7 fails, I will, but let's hope it doesn't come to that). Quote:

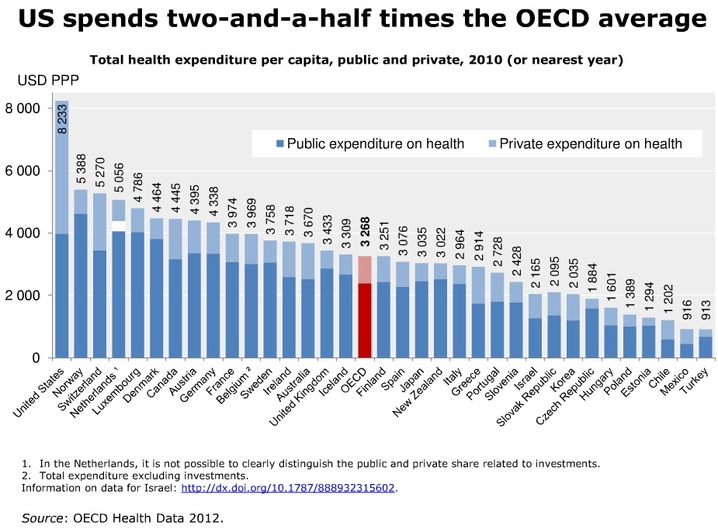

Who would turn down free medical care for everyone, anywhere? As I pointed out a few pages back, we're spending too high a percentage of GDP on medical care. If we could just reach the international average amongst the higher-developed nations, we could probably take a bigger step. Unfortunately, Obamacare does very little in terms of real health care reform. |

Quote:

Holy shit, motherfucker, can you read? Quote:

Quote:

1. I explicitly said I didn't think the situation applied to you or other FOFCers (and their ilk) who use these plans. 2. I didn't use the words "selfish" or "Un-American". 3. I was expressly making an explanatory post on the way medical benefits were used. :banghead: |

Quote:

It's unlikely that the increases were due to ObamaCare. Health care costs have risen 196% since 1999, with worker contributions rising 182%. Attributing an increase to ObamaCare simply neglects the reality of the historical ever-increasing health care costs. FYI, for those of us with families, the cheapest catastrophic $6k deductible plan would run about $600 back in 2009. I know, I looked. Those plans covered virtually nothing more than a wellness visit and picking up anything in excess of the $50 copay on prescriptions. And that didn't even cover maternity costs. So either your plan was extremely unusual, or... Quote:

...your plan didn't cover hardly anything. And since your insurance is now "insufficient", this confirms that your plan didn't amount to much at all. That's not an insult, but you must have had a very unusual plan. Quote:

So your near 100% in 5 years isn't much above the historical rise in costs for the last 14 years and you have added benefits. That sounds about right. Quote:

Are you still living in MI? On Michigan health insurance exchange: your state’s marketplace the lowest cost plan is $222 a month, not $303. Also, by your own admission, the new plans offer benefits that you do not currently have so you're not comparing apples for apples. Also note that MI chose not to launch it's own health care exchange and is riding off the federal one. States that launched their own have seen reduced costs. We do agree that health care needs to be reformed. I'm not a big fan of Obamacare because it doesn't fix the fundamental economic issues of health care. Goods that carry an inelastic demand typically don't work well without major government intervention. Unless we're willing to let people die on the street because they don't have access to health care, this is one of those industries that simply don't work well in a laissez faire marketplace. So unless we're willing to do that, there is no free market solution that fixes health care. Which is why that every other industrialized nation has gone to some sort of a single payer solutions, which provides roughly equal care (some things better, some worse - depending on the system) at far less of a % of GDP, which is good for everyone (except those who are raking in huge profits). |

Quote:

Huh? Blue Cross Premier Gold, which is BCBS's Gold plan on the Exchange in Michigan, costs $308/mo if you're under 50 for an individual plan or $525/mo if you're over 50 (prices lower for silver & bronze), includes a $150 in-network deductible and $300 out-of-network deductible with a $10,200 out of pocket maximum. Bear in mind those premium levels are without subsidies, but I'm going to assume you don't qualify for subsidies (though you might, if your ongoing FOF income is low or sporadic). It covers a variety of services out-of-network (see here). Quote:

Yeah you do. Again, in Michigan, just using Blue Cross as an example, the benefits are listed here (and those are the exchange plans, so you can buy them on the exchange or from BCBS direct), and you can look up individual providers, based on your plan here. Edit: Again, straight from the website, the Blue Cross Premier Silver Plan, which is available for $434/mo on the Exchange if you are over 50 and not eligible for subsidies, is a PPO with out-of-network coverage for most services: http://www.bcbsm.com/index/plans/mic...emier-ppo.html |

Quote:

As Blackadar noted, the increase is most likely due to rising health care costs, but let's look at those requirements that took effect in 2010 and 2011. They are: 2010 Coverage for children with pre-existing conditions Not applicable to you, probably didn't impact your plan, since your plan was individual-only (and thus so was its risk pool, presumably). Coverage for young adults under 26 Not applicable to you, probably didn't impact your plan, since your plan was individual-only (and thus so was its risk pool, presumably). No more lifetime limits on coverage Did you read your fine print? Did you have a lifetime limit in your beloved plan? Because this was reason #2 why catastrophic plans tended not to work if used as intended. No more arbitrary cancellations or rescissions And this is reason #1 why catastrophic plans tended not to work if used as intended. I am interested - did you ever use your plan for a catastrophe? What was your experience. Right to appeal health plan decisions Related to the above. Again, what did your fine print say? Consumer Assistance Program Not applicable to your plan. Small business tax credit Not applicable to your plan. Temporary coverage for people with pre-existing conditions Not applicable to your plan. Community Health Centers Not applicable to your plan 2011 Prescription drug discounts for seniors Not applicable to your plan. Free Medicare preventive services for seniors Not applicable to your plan, although arguably it should have made your plan (if used by seniors) cheaper. The 80/20 Rule (Medical Loss Ratio) Not likely to apply to your plan, since catastrophic plans are typically a very small part of an insurance company's revenue. They may have raised the premium to help their overall MLR, of course, but that's more an argument for the rising cost of health care causing the increase. Rate Review This could affect your premium if they decided to start pricing in future increases in current years. I would expect this, plus, as you said, they are preparing to discontinue the product (maybe for the Exchange catastrophic product?) means they now it's either actuarially unsound now, or it will be soon. In which case, ironically, it's the market working as intended. The brokers you are buying your insurance from are BS artists, Jim. |

Quote:

This is a relief. The web site indicates the premier plans have caps out-of-network. The file my agent sent me shows the opposite - calls them all HMOs. That concerns me. I definitely want to remain in a PPO. Remember that one of the complaints about the Obamacare web site so far is that the generic quotes are for over 50 and under 50, the under being if you're in your 20s. I am 48. Premier Silver would be $398. Premier Gold would be $481. Premier Bronze, which now does seem quite close to what I have (plus, apparently, maternal benefits) is $303. Is 300% over five years equivalent to what we see in health care costs? As for the motherfucker bit, if you were reading, you'd realize that paragraph was combining your words and others here. There is a definite mantra that people who have catastrophic plans are somehow gaming the system (yet Silver and Bronze are fairly close to catastrophic anyway). You may be right that they don't work as designed - I've never come close to the deductible. But they have helped in that there is a card and doctors have to filter their bills through BCBS. So I get a better rate than I would if I had no insurance. |

Quote:

I was trying (and failing) to channel my inner Samuel L. Jackson. I apologize. |

Quote:

You realize most liberals would like nothing better than that? The ACA is more of a compromise (heck, it was originally created by Republicans to begin with). |

Hey - I'm just glad we could help Jim see that he was receiving erroneous (to be kind) information from his insurance agents and that Obamacare might actually save him money, and certainly isn't going to cost him an obscene amount more.

Just goes to show though (I think we can all agree) that if you take the time to look at the reality yourself (all snark aside about how that's difficult since the website is apparently shite and all), it can actually be a positive thing for a lot of people. |

Quote:

I'd be first in fucking line to signup for universal single-payer, just out of principal. And I have a damn nice Tufts package I'd be giving up (I think my copay on office visits is like $25?) |

Quote:

And it's one that makes the insurance companies more, not less powerful. I never understood how that's a step towards single-payer, to have more private industry in healthcare. Sounds more like a Republican plan, which make sense because, ya. |

The bill we have now is a monumental piece of shit, whose full repercussions will not be felt for a couple more years. We're already seeing some of the cracks, and I seriously doubt it's going to improve.

*I'd* even wholeheartedly back a true universal single payer system...if it were not chock full of loopholes, partisan bullshit, fairy-tale costs, etc (much like the ACA). Unfortunately, our government incapable of such things. Even if a GOOD system could be proposed, it'd be heralded as the end of days by (insert party that didn't propose it here), and the ensuing war in Congress over it would turn it into...something like the ACA. "We have to do something" are the five most dangerous words one can hear from a congresscritter. |

Quote:

How will it save me money? In 2015, when I get dumped into the exchange, I will be paying in at least $1,400 per year more than I will in 2014. While I'm glad to find I can still go out of network, I would like to keep my existing plan. How do I make up the $1,400? That's a lot of money (especially when you haven't released a new game in several years). |

Quote:

Of course I realize that. The logical conclusion to the concept that health care is a right is a government absorption of the health care industry. I'm torn on that. I'm a social liberal, so I want people to have freedom to become whatever they work hard enough to become. But I'm a fiscal conservative, so I want to reform government. I think the practical solution is to reform health care, as monumental a task as that will be. Obamacare isn't just an expensive compromise; it refuses to even look at real reform in health care. Unfortunately, due to extraordinary mismanagement of the budget, we are not in a position to add entitlements. At some point, we have to pay for them. And our ability to pay is being reduced right now because of other unsound policies. |

i'm jealous of you folks who can use the website. it still has not worked for me - even to browse available plans (NJ)

|

Quote:

Again, what do you mean by reform healthcare? You, and a lot of people on the right say that, but there are rarely any specifics. |

Quote:

Another way to look at it is that the ACA merely brought forward your eventual (and inevitable) day of reckoning. The fact of the matter is that BCBS would have refused to renew your catastrophic plan at a point where you got old enough that you became an actuarial risk. Or, your day of reckoning would have been when you had a catastrophe and went backrupt. On the question of money, again I don't know how much you make (nor do I need to), but if it isn't a lot, you may qualify for a partial subsidy, especially if you look at coverage not from a single, but from a family (you got married, right?) standpoint. There are options, is what I'm saying. Quote:

Well, I think you answered your own question there.... :p |

Quote:

And you have to name 3 things that aren't tort reform or shopping across state borders. SI |

The notion of "healthcare reform" is one that has a really ugly truth: somebody somewhere is going to get royally fucked.

You can't "fix" it without dramatically reducing costs ... but there is little (or no) legitimate means for the government to get involved in that beyond what they negotiate for the patients the taxpayers are paying the freight for. Hypothetically, you can't just wave a magic wand & say "okay doctors, you can only charge $5 for service X" ... because they've invested (by incurring debt) based on the notion that there was a reasonable ROI. The problem with healthcare is that we've got too many people needing it, not enough money to pay for it and no legitimate or justifiable way to fix that. It is a royally fucked situation that likely has no "solution" that truly corrects that basic problem. The only "fix" will be when it collapses completely (likely moving things considerably toward solving that basic problem). |

Quote:

If by 'fucked' you mean curtailing the profits of the large health corporations which are milking the system presently - then yes I agree, however considering Americans pay out 2x the costs of most other modernized countries and receive less in return* I fail to see why individuals should be worse off if the reform is undertaken sensibly ... with regards to the ACA, its far to early to judge if its going to be a success at present in my opinion, we'll see in 5-10 years time how its viewed (I've seen a few interesting articles regarding how Medicare was initially viewed which mirror much of what has been said about the ACA today).  *By 'less' I mean not all the country is covered and there are higher out of pocket costs and far more red tape than is present in many other countries. |

Quote:

other countries have managed to come to some kind of solution (even if it's at the risk of lower quality) that has lower costs, so it must be possible. when you're the worst, it's hard to say that it can't be improved. |

Quote:

In my defense I did say "might" - I hadn't crunched the numbers. $1,400 a year is not nothing, but it's better than you thought, right? So maybe "won't cost as much more as you thought" is the more accurate phrase I should have used. |

I'd agree that bringing costs down radically now would screw over a lot of people, but we really don't have to do that. As bad as costs are now, they are sustainable if the growth rate in medical inflation is brought down significantly. We don't need to cut medical spending now, we need to reduce the amount of growth in medical spending over the next two decades. That can be done without very many people feeling they have gotten screwed.

|

Quote:

1. Through a Private set of companies, have a bare-bones "catastrophic" $6Kish deductible plan highly subsidized for all users through tax incentives. If you want to have it fully covered for people under 60K, I'm fine with that. But, it should be subsidized for all users. I don't care if you make $20K or $200K, everyone should be able to buy this level of coverage. This is the extend of the government interference. This coverage does not cover office visits, prescriptions, ... Just catastrophic coverage. There aren't 20 different levels with 9 different copays - it's one plan that everyone has fairly cheap access to. 2. Allow the purchase of an additional private plan that would add in doc visits, ER trips, prescription coverage,... Since everyone would have this initial "catastrophic" plan, the rates here shouldn't be outlandish. But, these plans will be expensive for people without employer provided coverage as health care IS EXPENSIVE. 3. Promote the crap out of the idea of health/medical expense account that is pre-tax. If you are a small business owner, maybe you go with the bare bones coverage of 1 and the cheapest option for 2 and set aside $3-4K a year in medical expense savings accounts. This would allow you to have a smaller monthly premium but still be able to go to the doc a handful of times a year and buy prescriptions with your pre-tax money. If you don't like that idea (or expect to have higher costs than normal), go with a better private plan with higher premiums. The end result here is to get people onto a "car insurance" style health care plan as their main plan and then allow them to pay more privately or get employer-provided plans for "premium" coverage. The main difference here is to have the government only involved in subsidizing (not providing, key difference) the high deductible catastrophic coverage plan. Once nearly everyone has that, a lot of things become more manageable. To really reduce costs, people would actually have to negotiate directly with doctors and hospitals to pay for services. Maybe some higher level private insurances would get you a discount, but you would still be paying for what you use in some capacity (no different than taking your car to the shop and the warranty covers some of the parts while you pay for labor and other parts on a negotiated price). But, we are a LONG way from that point. There's simply too much entitlement in the idea of health care in the US to get there anytime soon. |

Quote:

Are you keeping Medicare and Medicaid in roughly their current format or changing/cancelling those programs? |

Quote:

But wouldn't having the first items highlighted made available to more people help prevent having to claim the catastrophic insurance? Instead of heading issues off at the pass, they get ignored until you have to go in for catastrophic insurance. Going the route you are suggesting here seems penny-wise/pound-foolish. |

Quote:

|

Also, more preventative care results in less catastrophic coverage so you really should be promoting the former if you want to lower costs on the latter (though to really cause a sea change in reducing costs, delinking health ins from employment would be huge, because then the real costs would be seen of health care).

|

Even if you assume that the catastrophic plan pays for everything after the 6K deductible, that's a huge amount of money to ask people to pay if they are below the poverty line. There are a whole lot of people that aren't poor because they didn't save enough, they're poor because they don't make enough money to pay all the bills. That group is only going to get larger as machines replace more and more workers. How will your plan cope with these people?

|

Quote:

Not to mention the "moving goalposts" issue of his first paragraph. "Healthcare coverage" is whatever we decide to define healthcare coverage as, not what YOU Arles think it should be. |

Quote:

|

Quote:

|

Quote:

Yeah, this plan incentivizes waiting until medical problems are a catastrophe. Aren't most medical costs in the US either chronic disease management or end of life/trauma care? Will this plan even save a considerable amount of money? Certainly providers can adjust costs so that the cheaper stuff is even cheaper and the more expensive stuff is more expensive, thereby getting the government to pay more of the costs. |

Quote:

There is more to it than just annual physicals. It is going in to get something treated at the doctor's office before it turns into a hospitalization event. |

Quote:

|

Quote:

I don't know why death panels get such a bad rap. I say, bring 'em on! |

Quote:

You can shop around for a car at the price you can afford - or you can go without (sucks, but possible). You can shop around for an AC unit at the price you can afford - or you can go without (sucks, but possible). You can't shop around for the drugs or medical equipment you can afford, and in life threatening instances, you can't go without. |

Are their numbers on our overhead, i.e. how much of our health care spending goes to actually collecting and distributing the money, as opposed to directly providing care?

And getting people away from going to emergency rooms as their primary basic care will help a lot with costs. |

Quote:

So, what conditions are we afraid people won't go to the doc for if they elect a cheap private plan with $50-60 doc visits as opposed to $20 ones? |

Quote:

|

Quote:

I, for one, welcome our new death panel overlords. |

Quote:

What we are afraid of is if they elect to only go with the catastrophic plan, and not also one the cheap plans, which is an option you are providing. That changes nothing from how things are today, and part of the reason the ACA mandated minimum coverages for the plans. |

| All times are GMT -5. The time now is 06:59 PM. |

|

Powered by vBulletin Version 3.6.0

Copyright ©2000 - 2025, Jelsoft Enterprises Ltd.