|

|

Quote:

And when you develop a chronic condition and happen to get laid off and can't get new coverage because of your preexisting condition? What then? Just tough luck you're fucked and bankrupt? |

From a foreigner's perspective...

This Obamacare stuff already passed congress and was signed as a law in 2010? Basically, the Republicans are blocking the passage of a new budget in order to get this law modified? And the Democrats are refusing to compromise since they had already won the battle when this was still a series of Bills back before 2010? I suppose I don't understand how the US govt works, but are there no safeguards to the Federal Budget in case of political Partisanship? In the Philippines, if congress fails to enact a budget, the previoud year's budget is automatically grandfathered in, just to avoid the potential stoppage of Government services. |

Quote:

Nope - no safeguards, because we're silly. |

Quote:

Yuck, sounds like you have a stressful job. Imagine how many great employes your competitor can get if they are the only one to offer benefits. Those employees may be so great that their output would surpass that of the company filled with non-benefited employees. |

Quote:

It's a little late & I've had a long day buuuuut .... I think that would accomplish the same thing in the U.S. right now, since last year's budget would not have included funding Obamacare. Same as the basically everything but Obamacare budget that the House approved but the Senate rejected. |

The rhetoric among editorialists and press is so stupid. A professor of modern history is calling this the most extreme move in US history. I guess 1) since she only knows modern history, she wouldn't know about the Southern states seceding and 2) she probably doesn't know modern history that well if you act like this has never happened before.

Also, what's with the "mandate" about the election in saying it was all about the ACA? Everyone is implying that the election was about ACA vs. anti-ACA. That's stupid. I would bet that if Obama was anti-ACA, he still would have won. And even if Romney won, I would almost bet that ACA would still be in effect. There were several logical reasons why Obama won that went beyond ACA. |

Quote:

Not really, since Obamacare was the subject of a separate mandatory spending bill. That's why the House has to specifically defund Obambacare rather than fund it. |

Quote:

With the bonus of avoiding this silly mess. ;) |

It is a silly mess because it is the wrong fight. Unfortunately, there are many in DC that want to maintain the fiscal status quo and will not fight to change.

|

Quote:

I was reading about this recently. Until late in the Carter admin the government did continue at previous spending levels. Only after the Justice Dept wrote a series of opinions in 1980 did we get to the mess we have now. |

Quote:

We're fucked. |

I'm thinking no clean debt limit raise is > 90% probability at this point too FWIW.

Actually thinking I might put a bit of a short down on some of the domestic indexes in expectation of that.* *just my personal thinking, not an investment recommendation. |

Quote:

I wouldn't worry about that quote too much. He's just whistling past the graveyard there I believe. |

Quote:

Quote:

This would be a more effective argument if "employer coverage" tended to be "good coverage". Quote:

Um, actually, it would be better than what's available privately. Because what's available privately for free is, basically, nothing. Which is kinda the whole point of ACA. |

You all missed me. Especially EagleFan & JiMGA. Admit it. :p

|

Yes. But we need more diagrams!

|

Quote:

If you'd just stand still however ... ;) |

Wait? How did I miss an NFL in Pictures?!?

Oh, and hi, flere SI |

Quote:

Quote:

This...if that was a stick-figure GWB, I'd have enjoyed it MUCH more. |

Quote:

He hid it in the thread rather than breaking it out into its own like he used to. |

Quote:

That is pretty much how the US budget process works as well. But this current situation isn't related to a new budget, it is to raise the debt ceiling. They are basically agreeing to pay for things that the previous budget authorized. By raising the debt ceiling, they aren't adding more spending to the deficit. But, what the Tea Party Republicans are trying to do is to exact concessions before authorizing the government to pay for obligations that have already been authorized by Congress. |

Quote:

Isn't the current situation about the budget? The mess in 2 weeks will be about the debt ceiling. SI |

Quote:

Yeah i didn't want to say anything because his rant sounded so good even though the specifics were a little off. |

D'oh you are correct. They were so close to each other in timing, I had forgotten they were separate. But back to the point about a budget, they aren't voting on a new budget. They are voting on a continuous resolution, which keeps spending at the previous levels, which like the debt ceiling vote, doesn't add any new spending.

|

Quote:

As someone who also handles a lot of hiring and works with our HR, I see comparable benefits across the industry and we are certainly not any better than most companies out there. Intel, Honeywell, Motorola, Insight, On Semi - all have the same plan as we do. It's like congress, most Americans hate the "health care system" but are happy with their plan. Things do need to be improved, but our plans are very fairly priced for most of the working public. People happy with their Health Care don't go on the news and say "Yeah, I only had to pay $250 for a major surgery - seems fair to me". The issue is with people who don't have employer based coverage and that's where the effort should go initially. Quote:

|

Arles, the costs your employer pickup are pass-through. You can't just say that an employer is picking up the tab out of the goodness of their own heart. It's part of your salary. You are paying not only what your portion of the premium is, but what your employer picks up too.

Your employer is not subsidizing anything. |

Quote:

It's great that this is your experience, but the data paints a different picture: http://www.commonwealthfund.org/Publ...-and-2007.aspx Quote:

Another consequence: http://www.commonwealthfund.org/News...n-4-Years.aspx Quote:

Note both studies are from 2008, but cursory google searches indicate the trend continued to 2013. |

Quote:

This is the key point that people have been pointing out to him for a couple pages, but he seems to fail to grasp. |

Quote:

With regards to 'value' - two of my three kids were born in England, we paid $0 out of pocket for their births and time in hospital, the 'plan' had a monthly cost of around $450 for a family of 5 (ie. my NI contributions which incidentally was the maximum possible to make, if you were on minimum wage they'd be far less). Seeing a doctor in the UK costs $0 its a 'right', seeing a specialist costs $0 ... if you need medical drugs then you pay a fixed cost regardless of the cost of the drug involved (and if you're unemployed then the cost is waived) - please do note however that cosmetic surgery and suchlike isn't allowed under the NHS unless there is a damned good reason (i.e. serious burn victim etc.). With regards to the quality of the care, the US is pretty similar to what I've received in other countries (not just the UK, but elsewhere also) - they appear more 'test happy' over here and rarely see you on schedule (instead making you wait for 30 minutes to an hour past your appointment time), but thats about the only difference I've seen myself. I personally miss the reassurance I had in the UK that when a member of my family was ill all I hoped for was that they got better - in the US when someone is ill I also have to worry about what its going to cost us and whether its covered under the insurance plan we have ... even when it is the out of pocket expenses are ludicrous at times - I estimate I pay around $3-4k per year in out of pocket expenses for a family of 5 who are in the main very healthy ... thats on top of whatever SEGA are paying for the insurance itself. I know this affects a lot of peoples approach to medical care, I've friends I play football with who should be seeing doctors (they have niggling injuries) who don't because they feel they can't afford to - that to me shows something is wrong as it leads to people putting 'off' getting checked out until its too late and could be a serious issue. |

Quote:

Quote:

Quote:

|

The point was that you were arguing that you only pay $300 for a premium because your employer covers the other $400 while if you had to buy it on your own it would be $700. But you're paying $700 now, it's just not showing up on your pay stub. You aren't saving money by getting it through your employer.

And people absolutely see the benefit otherwise companies wouldn't do it. Why would a company provide a benefit if the employee didn't factor it into their decision? |

Quote:

Thats fine and obviously everyone has different choices and priorities, I liked the fact that the priority in Europe is to ensure everyone has access to quality medical care regardless of income level myself. I'm glad you're in a good place and are able to look after yourself and your family - thats awesome, however I personally believe EVERYONE should have access to quality medical care not just those who have good financial standing. You indicate a sweeping 'US employees get by far the best deal' - the well paid might do*, the lesser paid definitely don't in my opinion .... they get what they can often making do without health coverage at all. *I'd debate this as most American's I know are far more 'stressed' than English people I know - partially I believe because of the lack of a safety net, long hours working and the potential unpredictability of their outgoings (due to variable health costs etc.) ... there is more to life than raw cash imho and I think quality of life is the most important thing. |

I've been at places purported to have good insurance by both people inside and outside the company but I'm not certain that if I didn't suddenly have tk's health issues that I wouldn't be bankrupt right now.

SI |

Quote:

Quote:

Quote:

The ACA is setup to encourage companies to eventually drop covered employees as that will reduce the risk and reduce overall costs. There are some fines, but they don't have a ton of teeth when you look at the cost for providing benefits. Plus, the ACA would love more 25-45 year old middle class families with no serious health issues and stable jobs joining up. It's like having a car insurance company that covers only DUI offenders and then adding a bunch of perfect drivers. Over time, paying that $800 to $2000 fine is going to look very appealing compared to dolling out $400-$500 a month to cover certain levels of employees. I'm sure Execs and high paid will be fine, but the rank and file positions (unskilled, hourly, "replaceable" level) may lose their healthcare coverage and be forced to pay much more out of pocket for these exchanges. Again, time will tell, but I would have much preferred a system that completely excluded people with existing coverage for this phase (ir, make the fines more what it would cost to cover). Don't even give companies the carrot of considering cutting benefits or some will do so to save money. |

Oct 17 is the real D-day I think. I'll start the countdown

T-14 GOP legislator: Boehner won't let government default on its debt - CNN.com Quote:

|

Quote:

FYI, I brought it up as a reminder that the main purpose of ACA was to provide affordable health care for those who are currently uninsured or underinsured (and don't qualify for another government program). But I just noticed in your response to RainMaker about employer-based plans that you already recognized this, so I'll drop it. |

Quote:

I'll believe it when I see it. If he does so, I wonder how long it'll take Cantor to stab him in the back. |

Quote:

That's an interesting opinion, but I'm not sure what you're basing it on, other than your personal satisfaction with your company's policy and your sense that other companies have similar policies. That sort of anecdote doesn't really demonstrate anything other than the fact that some people have a policy they like. I've never seen a statistic that backs this idea up. Quote:

But who exactly is going to agree to cover a population of uninsured and pre-existing condition patients? The reason the two populations are being combined is that's how it makes economic sense. Nobody is going to take premiums only from sick patients and net a loss--by pairing them with patients who are generally healthy, they can charge a decent premium to everyone. Your suggestion seems to be that the government simply pay the health care costs for people who don't have good employer plans. I don't see how that's an improvement. Yes, you'd get to keep your cushy employer plan but certainly your taxes would increase. And now we'd have the government literally making health care decisions for anyone without a good plan, which is I think what a lot of people are trying to avoid. |

Quote:

Quote:

Quote:

They are setup as government program because they need to be heavily subsidized. I expect that the risk of covering pre-existing and some sick/low income people without access to employer-based coverage is also fairly risky. I would be fine setting up subsidized "exchanges" for these groups to ensure they have coverage options. Now, they may not be as cheap as what employer-insured people get, but they can be better than what's out there today. Quote:

1. Find a 40-hour job with employer-based coverage. 2. Find an insurance broker to get you a Co-OP or group coverage privately. 3. If neither 1 or 2 work for you (low income, pre-existing conditions, ...), we will have a government subsidized private health plan that is either state run or privately run (I'm fine either way) that you can join. Now, it probably will have a higher deductible than 1 or 2, an income ceiling to qualify (or pre-existing condition clause) and won't be as good a plan as employer-based because of the cost, but it will be an option. The key to option 3 is that there are limits to who can join (income level, pre-existing condition that prevents other coverage, ...). This is very similar to what Arizona has with ACCESS - you are just raising the income level a bit (to ensure part-time workers qualify) and adding in the pre-existing conditions piece. I also wouldn't have this completely paid for by the government, they would be subsidized on a scale based on the level of coverage people want and their income level. The difference between this and the ACA is that it stops at a certain income level (say $40K) to ensure it's not used as an out for companies that may be pondering taking a fine and using the ACA as a shield to save cash on benefits. Quote:

We have programs already setup in most states to cover the lower income families who need coverage. We just need to expand it slightly to cover those with pre-existing conditions and maybe raise the income level for who is eligible a hair to cover part-timers. I also think it shouldn't be fully covered once you get out of poverty. Maybe a sliding scale of % of premium paid by the person as their income level increases. This alone should cover a portion of the cost. This plan would be cheaper than the ACA as a significantly smaller % would need coverage. We can see how it does for a few years and as the uninsured decreases to a more minimal number, we could then decide if we want to try something completely different. |

Quote:

They've been doing it since 1986. Who do you think is footing the bill for the people who show up to a hospital without insurance? The people who show up with insurance. |

Quote:

As stated in the PBS article, 2016+ is when the middle class could really get hosed by the "unintended" consequences of the ACA on their coverage: Quote:

But maybe I'm wrong and in 2016-2018 no impact will occur to the millions and millions with affordable premiums offered through their employers now. It's just a risk that I don't feel is necessary if the goal is to initially reduce the number of uninsured. |

Those people with good jobs would be paying the taxes that subsidize your plan. I don't have a problem with your plan, it's in fact what Obamacare started out as in a way. I'm just saying that the people who are healthy and who get cheap, affordable insurance are going to be footing the bill no matter what. You're either paying it through higher premiums or through your taxes.

|

Quote:

I don't mind having small tax increases to cover safety net programs (which is where many conservatives and I differ). I just want transparency into why the increase occurs and steps to be taken to ensure spending doesn't go out of control because the government gets an extra 2% of our cash. I also think that limiting the program and providing some form of premium from the people in this public plan (ie, it's not just free) will help limit the cost over time. The reality is a lot of people that don't have insurance can go out and get a policy tomorrow with a $2K-5K deductible and not have it cost a ton out of pocket from a broker. It's not perfect, but it is insurance and protects them in the event of a massive 15-30+K hospital bill. Most just don't know how, don't think they need it or can afford it (ie, they check on a $250 or $500 deductible plan and are shocked at the cost). The only people who really "can't get" insurance are illegals and people with pre-existing conditions. For the latter, that's where some form of program should be instituted to help them. For the former, there's really nothing anyone can do to resolve this outside of some form of amnesty (which comes with its own problems). |

Interestingly, if you expand the polling sample beyond what is in Arles' link (only those who work for corporations with 2000+ employees were sampled, and only across 350 corporations), you find that while satisfaction with employer-provided plans remains high, the clear winner is Medicare: Reason-Rupe: 58 Percent of Americans Satisfied with Their Health Care; 23 Percent Dissatisfied - Reason-Rupe Surveys : Reason.com

That's great, but as my previous link showed (and this next link does too; and Arles' link does also), employer-based plans were already on the decline (both in terms of employers offering coverage, and the level of benefits offered) prior to the debate on ACA. It actually worse amongst small employers (which aren't surveyed by Arles' link, but are by mine). Rate of employer-based health insurance keeps dropping So, we're back to: Quote:

Is "most" employer-based coverage very good? Without a specific definition of "very good", it's hard to argue, but I'd be more comfortable with "good, but declining" based on the various links on offer, especially once one takes into account (as Arles' link does not), small employers, and knock-on effects from being underinsured on an employer-provided plan. Is it better than anywhere else in the world? We've done this to death previously, and it's easy to find research (starting here: World Health Organization ranking of health systems) - Wikipedia, the free encyclopedia, but in general, especially when compared to other first world countries, it's on par at best, but more generally worse overall. And when you add in the % of GDP spent on health care, it's clearly not a value proposition. Lastly, is it cheaper to the consumer? Well, no. It's not cheaper to the consumer when compared to any other single-payer system, unless you want to start arguing tax burdens, and even then you'd need to take into account the fact that US employers figure their contribution to your benefits as part of your salary, which is, in effect, a tax from a bottom-line perspective. In addition, as the studies I've shown have linked, one of the key problems with being underinsured (which is increasingly prevalent amongst those with employer-provided plans) is financial stress. Financial stress, in this instance, is due to lack of predictability of medical costs, which happens amongst the underinsured when high deductibles and out-of-pockets happen, which are increasingly the case (see also: High Deductible Health Plans). If you then combine satisfaction with a plan (see also: http://www.deloitte.com/assets/dcom-...bal_062111.pdf for a global perspective) with cost of a plan to a consumer, making a case that the end-state of health care coverage for middle-to-upper class white collar workers with employer-provided coverage (because that's what we're talking about here, mainly) is clearly, plainly and significantly superior to other coverage provided worldwide is, in my opinion, not a case well-supported by data. |

Borrowed from Facebook, but I thought this was funny....

GOVERNMENT SHUTDOWN AS COULD BE EXPLAINED TO A CHILD: GOP: Can I burn down your house? POTUS: No GOP: Just the 2nd floor? POTUS: No GOP: Garage? POTUS: No GOP: Let's talk about what I can burn down. POTUS: No GOP: YOU AREN'T COMPROMISING |

Quote:

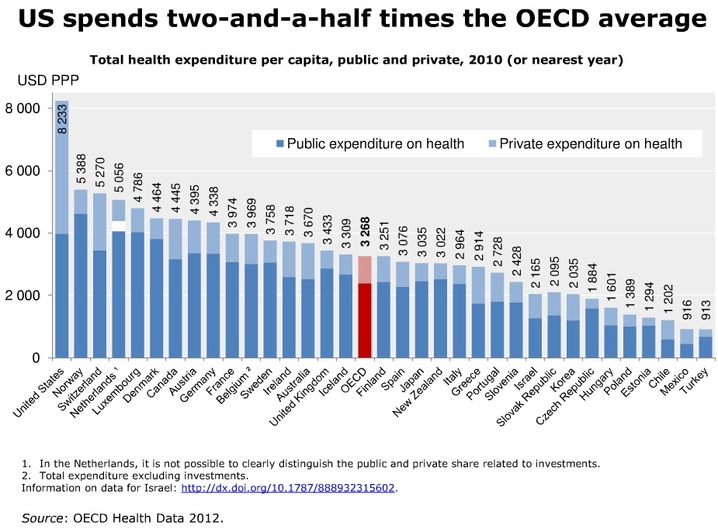

Cost is really easy. We spend way more per capita on healthcare than any other country. Hell, we spend close to most of the industrialized world just in government spending.  |

The problem becomes as to whether people think their tax burden going from 25-35% and increasing to 45-50% (Canada/UK/Europe rates) is worth the supposed "improvements" to their individual health care plans. I doubt many people with fulltime jobs ranging from 45K-100K upward would be excited to pay an extra 6K to 20K in taxes every year just to have some form of universal coverage that is likely not going to be as high a quality as the coverage they currently have.

Now, if you have a solution that does not either involve massive monthly premium increases or tax increases for working people, I'm all ears. Otherwise, I don't see the need to massively increase someone's tax burden or premium to solve a problem that doesn't exist for them. My advice is try to fix the actual problem of uninsured (mostly pre-existing, lower income and part-time workers not understanding their options), not add a massive tax/premium burden to the middle class with employer-based coverage. |

Quote:

:D |

Whats wrong is that in FL the servers are crashed from all those people who dont want Obamacare.

|

Quote:

What's interesting about that graph is despite the fact that the US has lower wait times for surgery, higher overall quality of care and lower cost to the consumer (when taxes are figured in), the public cost is roughly on par with that in Europe or Canada. I'd also be interested in factoring the additional tax burden on citizens to have the decreased public cost. If the US increased their tax rate to 45% for everyone like the UK to have a public health system - I'm sure the overall costs would go down. Of course, then a normal fulltime worker making 60K who paid $3.5K pre-tax in yearly premiums and another $1K in pretax expenses would now save that money but be facing a tax increase of between $8 and $10K a year. Not exactly saving them money...especially when you factor in it's doubtful they would have the same quality of care options they do now. |

| All times are GMT -5. The time now is 04:51 AM. |

|

Powered by vBulletin Version 3.6.0

Copyright ©2000 - 2025, Jelsoft Enterprises Ltd.